Chief Executive Officer, Gerald M. Soloway addresses company investors and executives during the Home Capital Group Inc. Annual General Assembly held at the Design Exchange in Toronto on Tuesday, May 18, 2011.

THE CANADIAN PRESS/Aaron Vincent Elkaim

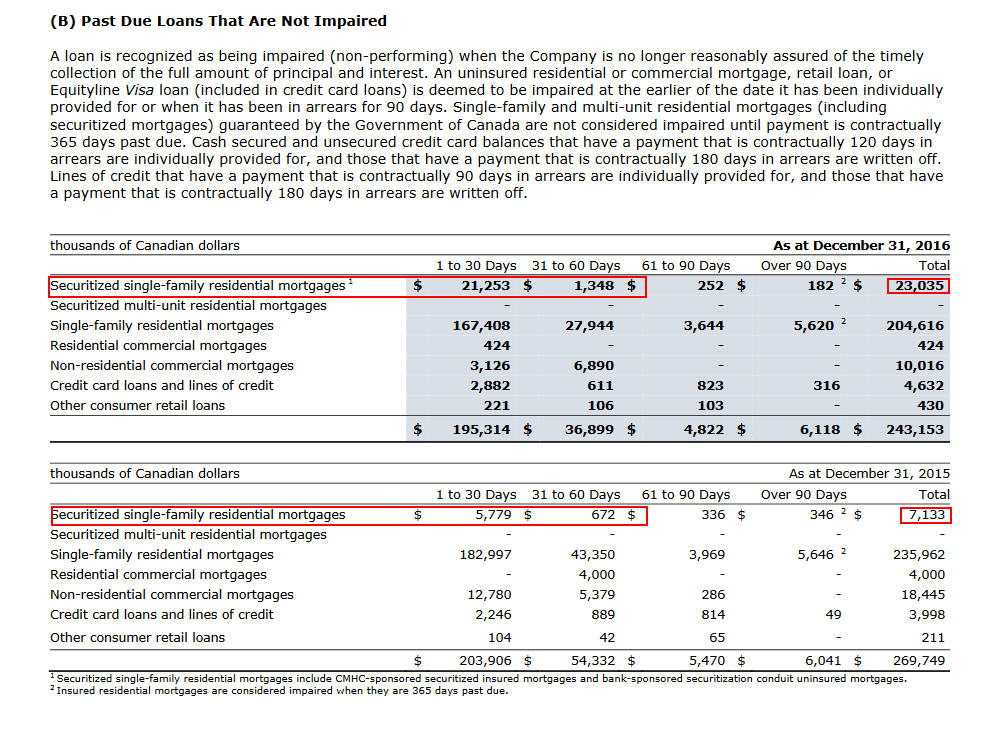

Wednesday, April 26, 2017 is a day that will forever be etched in the memories of Home Capital Group shareholders. In a span of a few hours, the company’s stock plunged 65 percent — it started the trading day at $17 per share, and closed at $5.99. One of Canada’s biggest mortgage lenders, once valued at $2.5 billion, was reduced to a mere $350 million. Thousands of Canadians were faced with a scary prospect — what’s going to happen to my mortgage if Home Capital goes bust?A week earlier — April 19, 2017 — the Ontario Securities Commission released a series of scathing allegations against Home Capital’s business practices. The allegations, the result of an 18 month-long investigation by the OSC, concluded that Home Capital made “materially misleading statements” to its shareholders, blaming the decline in its mortgage business to “external vagaries, such as seasonality and competitive markets.” In fact, it was internal fraud that was depleting Home Capital’s bottomline.The OSC’s statement sent shockwaves through a mortgage industry already reeling from the impact of tighter lending requirements. By Friday, April 28, investors were fleeing — the company’s high interest savings deposit balances dropped to approximately $500 million, from $2 billion.In February 2015, it was discovered that more than 30 mortgage brokers affiliated with Home Capital were inflating the incomes of mortgage applicants, a practice that is called “bad underwriting”. It is estimated that these brokers brought in $880 million worth of mortgages in 2014 alone, 10 percent of the overall number of mortgages brought in by all of Home Capital’s brokers.While that was big money, it was unfortunately obtained through illegal means. When this information finally made it to the top of Home Capital’s corporate ladder, CEO Gerald Soloway ordered an internal investigation which resulted in the firing of 30 brokers, 4 underwriters and 2 brokerages.Because Home Capital’s revenue (at least for their mortgage portfolio) was quite heavily dependent on the illegal methods of these particular employees, the company started suffering financially. They reduced their monetary targets dramatically, but insisted that it had nothing to do with the income fraud mess.They instead blamed “macroeconomic factors”. Odd, considering the positive housing climate — booming demand, and low interest rates.Business went on as usual, and by April 2016, Home Capital’s stock had actually risen back up to the level it was before the fraud fiasco.According to the OSC, in a mid-2015 conference call, an analyst pushed the idea that Home Capital was on the brink of a crisis.[“Okay. So it was –okay, so it was a little bit of teething pains. But were you guys being a little more cautious on underwriting? I’m just trying to get a sense of, has it been because maybe brokers have been losing some market share, whether or not it’s been small competition within the broker channel or to…”Soloway replied, “None of that has changed. I think it’s very similar to what it was last year. There isn’t a dramatic one quarter change. There’s been no new competitor. There’s been no new change in brokers. Brokers are exactly the same in my estimate.”]“People knew about the fraud, it was out there in the media, but the tipping point was the fact that management lied to their shareholders about it,” James Thorne, a money manager at Caldwell Investment told VICE Money. Thorne used to own a piece of Home Capital’s pie, but sold his holdings over two years ago, after learning about its bad underwriting practices.“I don’t own any Canadian mortgage companies, or any Canadian banks. There’s too much risk involved. I think people aren’t standing back and saying look, what happened at Home Capital might be an industry-wide problem.”Handing out mortgages like candyIf Home Capital’s shoddy underwriting practices are indeed an isolated incident, confined to one lending institution that in fact, makes up less than one percent of Canada’s mortgage market, then there really isn’t anything to fret about.But consider a scenario where more than one financial institution started issuing mortgages to people who potentially couldn’t afford to pay them back.“35 percent of the TSX is exposed to the real estate industry. Canadian household debt is at 167 percent of disposable income. We have an over-extended real estate market and an economy with a large amount of leverage. And now, we have our first piece of evidence of bad underwriting in the mortgage industry,” Thorne said.This particular broker worked in tandem with a real estate agent, who also chose not to be named. Their target market? Young Canadians, mostly downtown Toronto renters who were keen to get a foot into the real estate door, but had previously been rejected by the big banks for having not met the criteria to receive a mortgage. “That’s the role of a mortgage broker, though,” the broker told VICE Money. “It’s tough out there for freelancers, and banks make it very difficult for people to get mortgages. We want to help people own a home.”“The real question is how many Canadian financial institutions are handing out mortgages to people who shouldn’t be holding them?” asks Thorne. “We don’t know, and that’s a problem. But having lived through the 2007/2008 financial crisis in the U.S., I’m pretty skeptical that only one company [Home Capital] has bad underwriting practices.”Much ado about nothing?According to February 2017 data from the Canadian Bankers Association, the delinquency rate of all residential mortgages in Canada stands at 0.28 percent. There are currently 4.7 million mortgages in the Canadian housing market — only 13,000 of those mortgages have payments overdue by more than 365 days. At the height of the financial crisis, the delinquency rate of U.S. residential mortgages was 11.5 percent.Toronto realtor David Fleming brushes off the theatrics of Home Capital pessimists. “The media loves talking about things that aren’t there. They have accurately predicted 12 of the last two recessions,” he joked to VICE Money over the phone.“This is a stock market story, not a real estate story. There won’t be any kind of huge fallout in the mortgage market. This speculation and negativity is primarily from market bears looking for the opportunity to short Canadian real estate.”His views are echoed by one of Canada’s best housing economists, Benjamin Tal. “This is not a turning point for the market. It [Home Capital] is a very, very small segment of the market and this is definitely not the beginning of the end like people are saying.”Containing the falloutThere are rumblings that Home Capital’s financial situation is even worse than what’s publicly known. At the end of April the company took out a $2 billion line of credit from the Healthcare of Ontario Pension Plan (HOOPP). On May 2nd, the company postponed the release of its latest financial results to recruit new board members, in a bid to shore up credibility, stem negative commentary, and potentially find a buyer for its assets.An analysis of Home Capital’s 2016 annual report shows us that as of December 31, 2016, there were at least $23 million worth of securitized single-family residential mortgages that were late on payments. That’s in contrast to $7 million in 2015, perhaps a sign that more borrowers are having difficulty making their payments. If Home Capital gets bought out, it cannot be guaranteed that its clients will be subject to the same terms that they currently hold their mortgages at. Depending on how severe Home Capital’s financial situation really is, mortgage holders could be in for a rough ride.“Does a bank buy the mortgage assets? Or will it be a vulture hedge fund? And what will they do with mortgages in arrears? Will they basically put all those houses on the market to get their money back? You’d better hope it’s a big bank, because they are much more open-minded to helping clients,” concluded Thorne.

If Home Capital gets bought out, it cannot be guaranteed that its clients will be subject to the same terms that they currently hold their mortgages at. Depending on how severe Home Capital’s financial situation really is, mortgage holders could be in for a rough ride.“Does a bank buy the mortgage assets? Or will it be a vulture hedge fund? And what will they do with mortgages in arrears? Will they basically put all those houses on the market to get their money back? You’d better hope it’s a big bank, because they are much more open-minded to helping clients,” concluded Thorne.

Advertisement

Investors, it turns out, were spooked by the no-holds-barred tone of the OSC that accused a trio of top executives at Home Capital for deliberately covering up the fact that mortgage brokers were committing fraud — forging incomes of mortgage applicants in order to ensure that they would qualify for Home Capital mortgages.Capitalizing on bad creditHome Capital Group is the holding company of Home Trust, which provides Canadians a range of credit options including mortgages, lines of credit, and credit cards. Unlike borrowing from one of the big five Canadian banks, it’s much easier for the average borrower to be eligible for a Home Capital credit product. This is simply because Home Capital targets Canadians who usually wouldn’t qualify for a mortgage from a bigger lending institution like Scotiabank or TD.More than 30 of Home Capital’s mortgage brokers were inflating the incomes of mortgage applicants

Advertisement

But then the OSC allegations came out, scorching the credibility of Home Capital’s executives.“I don’t own any Canadian mortgage companies, or any Canadian banks.”

Advertisement

Advertisement

Indeed, the Canadian Housing and Mortgage Corporation has strict rules that govern the eligibility requirements to obtain a mortgage. But to a large extent, the CMHC relies on compliance by lending institutions. These lenders however, are insured by the CMHC — if you can’t afford to make your mortgage payments for more than a year, the CMHC will step in on your behalf. That, in a sense, gets lenders off the hook, and allows them to take more risks by tweaking the eligibility requirements for big loans.“We know everyone is doing it,” a Toronto-based mortgage broker who refused to be named told VICE Money. “I had clients who were freelancers, and didn’t have a steady income, but I trusted they had the financial backing of their parents so we would use their parents’ income to qualify them for a mortgage.”“The real question is how many Canadian financial institutions are handing out mortgages to people who shouldn’t be holding them?”

Advertisement

There are rumblings that Home Capital’s financial situation is even worse than what’s publicly known.

Advertisement

Advertisement

And then you have the hundreds of Home Capital employees whose jobs are on the line. Regardless of whether the company actually goes broke, there is a strong chance it will be bought out and restructured, potentially leading to job losses.“I know I’m not going to get my bonus this year. Within the company they tell us everything is okay, and I guess that makes me feel a bit better, but then I read the headlines and I get worried,” one employee told VICE Money. The employee refused to be named for fear of being fired by Home Capital for talking to the media.On some level, says James Thorne, we Canadians are the architect of our own misery.“We came out unscathed from the financial crisis, and then we started attracting all this international capital to Toronto and Vancouver because, look, they trusted our banking system. Let’s hope they are right.”With research files from Nathan MunnFollow Vanmala on TwitterWe Canadians are the architect of our own misery